Las Vegas Housing Prices Reached the Highest Level in the Last 11 Years According to LasVegasRealEstate.org

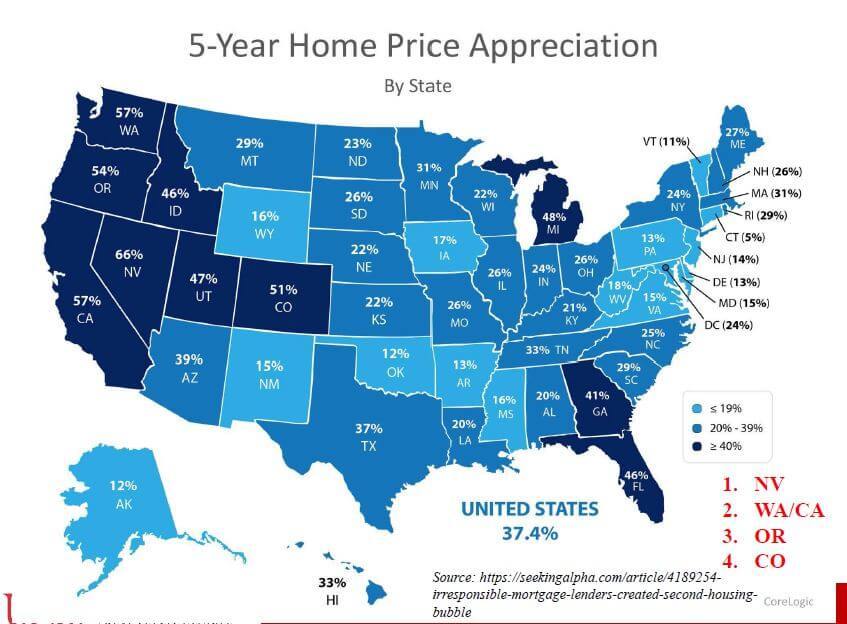

LAS VEGAS, November 16, 2018 (Newswire.com) - Real estate experts have marked a significant change in the economy and housing prices in Las Vegas during the last couple of months. 2018 has brought many changes to the Las Vegas real estate market, with prices rising rapidly and the number of available properties dropping just as quickly. However, it is certain that the city of Las Vegas is booming once again after the massive market crash in 2008. According to Nevada Current and the statistics from August 2018, the average price of a single-family home in the area of Southern Nevada equaled to $295,000. This shows how the prices have increased significantly since 2012 when the same properties were available for $118,000. However, even today’s average is still below the all-time high, which was $315,000, back in June 2006.

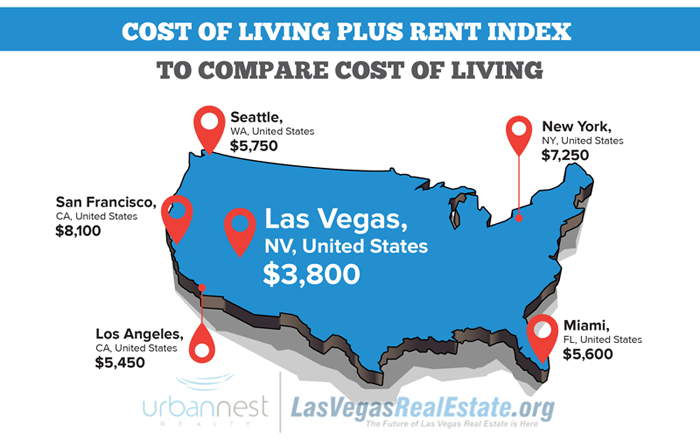

William Margita, a recognized industry leader and REALTOR at Urban Nest Realty says, “Despite being one of the fastest growing markets in the United States, the property values in Las Vegas are still below the average pricing of major U.S. cities and half the price of California.” The fact that Las Vegas offers lower costs of living and has no state income tax has contributed to the rapid increase in population over the last decade. This makes Las Vegas a great opportunity for those looking to find a permanent home at affordable prices, yet keep the luxury and convenience of living in even a guard gated community like the Las Vegas Country Club where condos still start at $120,000 and homes for $300,000. Margita adds the 30 percent of buyers are currently coming from California where they may be selling a Million dollar home, then buying a comparable property for half the money in Las Vegas and taking advantage of the cost-of-living ratios and active lifestyle.

The property values in Las Vegas are still below the average pricing of major US cities...

William Margita, REALTOR - Urban Nest Realty

Chris Bishop, the president of the Greater Las Vegas Real Estate Association, added that the prices of single family homes fell for 6.6 percent compared to the previous year, while the prices of condos and townhouses went up for 11 percent. This fluctuation in the market could indicate that the trend is about to rise again. “At the rate we’re going, with prices going up by nearly $5,000 per month, it’s possible that local home prices could finally get back to their all-time peak sometime later this year,” added Bishop, the president of GLVAR, in June of 2018. The Nevada Independent further explained that, at the rate things are currently going, the housing prices could even grow above the all-time record of 315,000$ in the first quarter of 2019.

Besides the slight fluctuation seen throughout May, June, and August, there are plenty of other factors that make Las Vegas real estate an interesting and quite diverse market. With the city constantly expanding, the demand for housing never seems to drop. Buyers are searching for properties on a daily basis, either looking for a permanent home or a profitable investment. The same source at The Nevada Independent tells us that apartment vacancy and rental inventory in Las Vegas has been declining since 2011. The fact that housing prices are increasing is going to benefit the rental market in the area, as more people are going to opt for renting in order to manage their budget increasing the profit for those who invested in rentals. One such market is Summerln, located to the west of Las Vegas, in which there are currently less than 96 Summerlin Condos for sale in the largest master planned community in Las Vegas.

According to the most recent analysis from the Lied Institute for Real Estate at UNLV, the apartment vacancy rate equals to 7.2 percent, while rental prices jumped from 876$ in 2008 to an average of 1003$ today. Furthermore, News Las Vegas confidently confirmed that the Las Vegas real estate market is indeed the hottest market in the nation. The recent changes in the pricing resulted in a value increase of 13 percent compared to last year. Besides new communities and complexes, the city is constantly growing richer in businesses, companies, and projects, which opens up new opportunities for people all over the nation.

Other sources such as the Review Journal also confirmed that the Las Vegas property prices are growing at one of the fastest rates in the country. With that said, if you were planning to sell a property, now would be the time to do so, as the values are about to reach the peak again. With the property demands rising, builders are competing to increase the availability of properties in the city, providing buyers with a wider variety of options. However, the president of GLVAR stated that the number of available housing properties is not even close to where it should be, as it will take a lot of work to meet such a rapidly growing demand. This might be an indicator that this real estate market is about to surpass its highest value ever recorded in 2006.

Las Vegas is already ranked number one by numerous reputable sources as one of the best cities to live in. The biggest question is whether these rising prices are going to scare the buyers away? While there is a possibility that the rapid increase in value might make some buyers abandon the idea of purchasing a Las Vegas property, it might also motivate others to make their move faster and secure a good property at a good price. Waiting only a few months longer could mean losing a great opportunity, as most real estate experts are expecting the prices to go even higher in 2019. For more information on the current Las Vegas real estate market, see www.LasVegasRealEstate.org.

Source: LasVegasRealEstate.org

Related Media