Global Agricultural Robots and Drones Forecasts 2018-2038: Technologies, Markets and Players

BOSTON, June 28, 2018 (Newswire.com) - The recent market report Agricultural Robots and Drones 2018-2038: Technologies, Markets and Players from business intelligence firm IDTechEx Research analyses how robotic market and technology developments will change the business of agriculture, enabling ultra-precision and/or autonomous farming and helping address key global challenges.

It develops a detailed roadmap of how robotic technology will enter into different aspects of agriculture, how it will change the way farming is done and transform its value chain, how it becomes the future of agrochemicals business and how it will modify the way we design agricultural machinery.

In particular, Agricultural Robots and Drones 2018-2038: Technologies, Markets and Players provides:

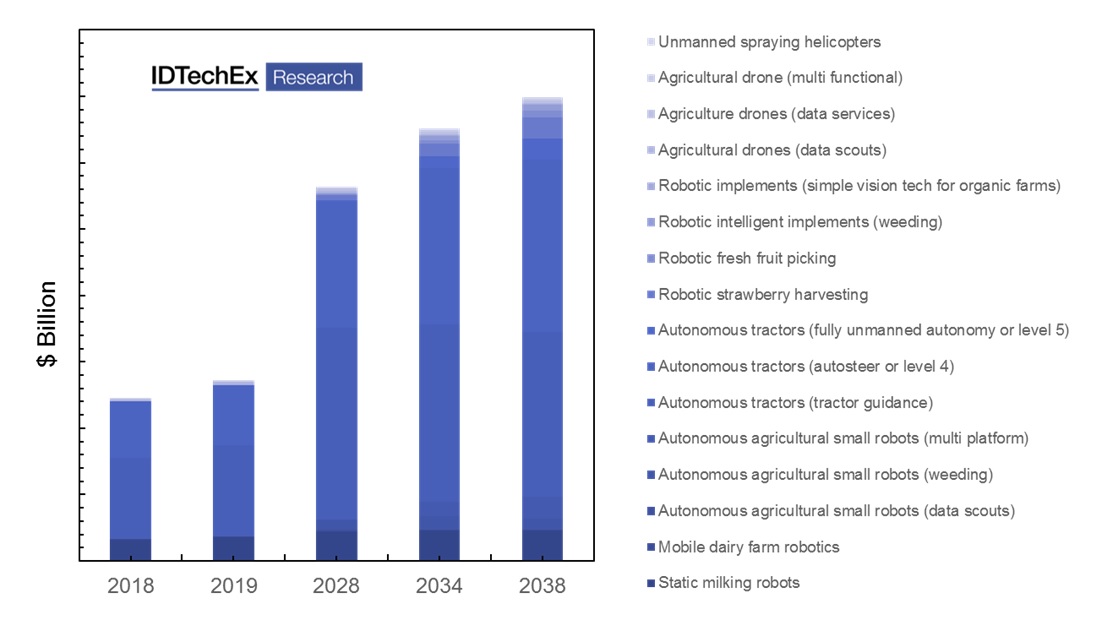

Market forecasts: The report provides granular twenty-year (2018-2038) market forecasts for 16 market categories. IDTechEx built a twenty-year model because their technology roadmap suggests that these changes will take place over long timescales. The market forecasts are often segmented by territory. All assumptions and data points are clearly explained.

More specifically, the report covers the following 16 categories: static milking robots, mobile dairy farm robotics, autonomous agricultural small robots (data scouts, weeding and multi-platform), autonomous tractors (simple guidance, autosteer, fully unmanned autonomy), robotic implements (simple and highly intelligent), robotic strawberry harvesting, robotic fresh fruit picking, and agricultural drones (data scouts, data services/analytics, multi-functional drones, unmanned spraying helicopters).

Technology assessment: A detailed technology assessment is included covering all the key robotic/drone projects, prototypes and commercial products relevant to the agricultural sector. Furthermore, the report offers an overview and assessment of key technological components such as vision sensors, LIDARs, novel end-effectors, and hyper/multi-spectral sensors. Technology roadmaps also outline how different equipment is increasingly becoming vision-enabled, intelligent and unmanned/autonomous.

This report also analyses the key enabling hardware and software technologies underpinning new robotics. For the hardware part, long-term price and performance trends in transistors, memory, energy storage, electric motors, GPS, cameras, and MEMS technology are considered. For the software side, the latest achievements in deep learning applications in various fields are covered.

Application assessment: A detailed application assessment covering dairy farms, fresh fruit harvesting, organic farming, crop protection, data mapping, seeding, nurseries, and so on. For each application/sector, a detailed overview of the existing industry is given, the needs for and the challenges facing the robotic technology are analyzed, the addressable market size is estimated by territory, and granular ten-year market projections are given.

Company profiles: More than 20 interview-based full company profiles with detailed SWOT analysis, 45 company profiles without SWOT analysis, and the works of more than 80 companies/research groups listed and summarized.

Will tractors evolve towards full unmanned autonomy?

Tractor guidance and autosteer are well-established technologies. In the short to medium terms, both will continue their growth thanks to improvements and cost reductions in RTK GPS technology. Indeed, IDTechEx Research estimate that around 700k tractors equipped with autosteer or tractor guidance will be sold in 2028. They also assess that tractor guidance sales, in unit numbers and revenue, will peak around 2027-2028 before a gradual decline commences. This is because the price differential between autosteer and tractor guidance will narrow, causing autosteer to attract more of the demand. Note that the model accounts for the declining cost of navigational autonomy (e.g., level 4 for autosteer).

Unmanned autonomous tractors have also been technologically demonstrated with large-scale market introduction largely delayed not by technical issues but by regulation, high sensor costs and the lack of farmers' trust. This will start to slowly change from 2024 onwards. However the sales will only slowly grow. IDTechEx Research estimate that around 40k unmanned fully-autonomous (level 5) tractors will be sold in 2038. The uptake will remain slow as users will only slowly become convinced that transitioning from level 4 to level 5 autonomy is value for money. This process will be helped by the rapidly falling price of the automation suite.

Overall, the model suggests that tractors with some degree of autonomy will become a $27Bn market at the vehicle level (our model also forecasts the added value that navigational autonomy provides).

The rise of fleets of small agricultural robots

Autonomous mobile robots are causing a paradigm shift in the way we envisage commercial and industrial vehicles. In traditional thinking bigger is often better. This is because bigger vehicles are faster and are thus more productive. This thinking holds true so long as each vehicle requires a human driver. The rise of autonomous mobility is however upending this long-established notion: fleets of small slow robots will replace or complement large fast manned vehicles.

These robots appear like strange creatures at first: they are small, slow, and lightweight. They therefore are less productive on a per unit basis than traditional vehicles. The key to success however lies in fleet operation. This is because the absence of a driver per vehicle enables remote fleet operation. The IDTechEx Research model suggests that there is a very achievable operator-to-fleet-size ratio at which such agrobots become commercially attractive in the medium term.

We are currently at the beginning of the beginning. Indeed, most examples of such robots are only in the prototype or early stage commercial trial phase. These robots however are now being trailed in larger numbers by major companies, whilst smaller companies are making very modest sales. The inflection point, IDTechEx suggests, will arrive in 2024 onwards. At this point, sales will rapidly grow. These small agrobot fleets themselves will also grow in capability, evolving from data acquisition to weeding to offering multiple functionalities. Overall, IDTechEx Research anticipate a market as large as $900M and $2.5Bn by 2028 and 2038, respectively. This will become a significant business but even it will remain a small subset of the overall agricultural vehicle industry.

Implements will become increasingly intelligent

Implements predominantly perform a purely mechanical functional today. There are some notable exceptions, particularly in organic farming. Here, implements are equipped with simple row-following vision technology, enabling them to actively and precisely follow rows.

This is however changing as robotic implements become highly intelligent. Indeed, early versions essentially integrated multiple computers onto the implement. These are today used for advanced vision technology enabled by machine learning (e.g. deep learning). Here, the intelligent implements learn to distinguish between crops and weeds as the implement is pulled along the field, enabling them to take site-specific weeding action.

IDTechEx Research anticipate that such implements will become increasingly common in the future. They are currently still in their early generations where the software is still learning, and the hardware is custom built and ruggedized by small firms. Recent activities including acquisitions by major firms suggest that this is changing.

Robotics finally succeed in fresh fruit harvesting?

Despite non-fresh fruit harvesting being largely mechanized, fresh fruit picking has remained mostly out of the reach of machines or robots. Picking is currently done using manual labour with machines at most playing the part of an aid that speeds up the manual work.

A limited number of fresh strawberry harvesters are already being commercially trialled and some are transitioning into commercial mode. Some versions require the farm layout to be changed and the strawberry to be trained to help the vision system identify a commercially-acceptable percentage of strawberries. Others are developing a more universal solution compatible with all varieties of strawberry farms.

Progress in fruit picking in orchards has been slower. This is because it is still a technically challenging task: the vision system needs to detect fruits inside a complex canopy whilst robotic arms need to rapidly, economically and gently pick the fruit.

This is however beginning to change, albeit slowly. Novel end effectors including those based on soft robotics that passively adapt to the fruit's shape, improved grasping algorithms underpinned by learning processes, low-cost good-enough robotic arms working in parallel, and better vision systems are all helping push this technology towards commercial viability.

IDTechEx Research forecast that commercial sales- either as equipment sales or service provision- will slowly commence from 2024 and that an inflection point will arrive around 2028. They suggest a market value for $500M per year for fresh fruit picking in orchards.

Drones bring in increased data analytics into farming

Agriculture will be a major market for drones, reaching over $420m in 2028. Agriculture is emerging as one of the main addressable markets as the drone industry pivots away from consumer drones that have become heavily commoditized in recent years.

Drones in the first instances bring aerial data acquisition technology to even small farm operators by lowering the cost of deployment compared to traditional methods like satellites. This market will grow as more farmers become familiar with drone technology and costs become lower. The market will also change as it evolves: drones will take on more functionalities such as spraying and data analytic services that help farmers make data-driven decisions will grow in value.

Note that the use of unmanned aerial technology is not just limited to drones. Indeed, unmanned remote-controlled helicopters have already been spraying rice fields in Japan since early 1990s. This is a maturing technology/sector with overall sales in Japan having plateaued. This market may however benefit from a new injection of life as suppliers diversify into new territories

Robotics in dairy farms is a multibillion dollar market already

Thousands of robotic milking parlours have already been installed worldwide, creating a $1.6bn industry. This industry will continue its grow as productivity is established. Mobile robots are also already penetrating dairy farms, helping automate tasks such as feed pushing or manure cleaning. In general, this is a major robotic market about to which little attention is paid.

For more on agricultural robotics and drones visit www.IDTechEx.com/agri.

Media Contact:

Charlotte Martin

Marketing & Research Co-ordinator

c.martin@IDTechEx.com

+44(0)1223 812300

Report Table of Contents

1. |

EXECUTIVE SUMMARY |

1.1. |

What is this report about? |

1.2. |

Growing population and growing demand for food |

1.3. |

Major crop yields are plateauing |

1.4. |

Employment in agriculture |

1.5. |

Global evolution of employment in agriculture |

1.6. |

Aging farmer population |

1.7. |

Trends in minimum wages globally |

1.8. |

Towards ultra precision agriculture via the variable rate technology route |

1.9. |

Ultra Precision farming will cause upheaval in the farming value chain |

1.10. |

Agricultural robotics and ultra precision agriculture will cause upheaval in agriculture's value chain |

1.11. |

Agriculture is one the last major industries to digitize: a look a investment in data analytics/management firms in agricultural and dairy farming |

1.12. |

The battle of business models between RaaS and equipment sales |

1.13. |

Transition towards to swarms of small, slow, cheap and unmanned robots |

1.14. |

Market and technology readiness by agricultural activity |

1.15. |

Technology progression towards driverless autonomous large-sized tractors |

1.16. |

Technology progression towards autonomous, ultra precision de-weeding |

1.17. |

Technology and progress roadmap for robotic fresh fruit harvesting |

1.18. |

20-year market forecasts (2018 to 2038) for agricultural robots and drones segmented by 16 technologies |

1.19. |

Summary of market forecasts |

1.20. |

Tractors evolving towards full autonomy: 2018-2038 market forecasts in unit numbers segmented by level of navigational autonomy |

1.21. |

Tractors evolving towards full autonomy: 2018-2038 market forecasts in market value segmented by level of navigational autonomy |

1.22. |

Tractors evolving towards full autonomy: 2018-2038 market forecasts segmented by level of navigational autonomy (value of automation only) |

1.23. |

The rise of fleets of small autonomous robots: 2018-2038 market forecasts in unit numbers segmented by level of robot functionality |

1.24. |

The rise of fleets of small autonomous robots: 2018-2038 market forecasts in market value segmented by level of robot functionality |

1.25. |

Robotic tractor-pulled implements become increasingly intelligent and multi-functional: 2018-2038 market forecasts |

1.26. |

Robotic fresh fruit harvesting will overcome challenges but only in the long run: 2018-2038 market forecasts for robotic fresh fruit harvesting |

1.27. |

Agricultural drones become multi-purpose and data services capture more value: 2018-2038 market forecasts |

1.28. |

Robotic milking are already a major market: 2018-2038 market forecasts |

1.29. |

Mobile robots and drones dominate the agricultural robotic market: 2018-2038 market forecasts segmented by mobility vs stationary robots |

2. |

AUTONOMOUS MOBILITY FOR LARGE TRACTORS |

2.1. |

Number of tractors sold globally |

2.2. |

Value of crop production and average farm sizes per region |

2.3. |

Revenues of top agricultural equipment companies |

2.4. |

Overview of top agricultural equipment companies |

2.5. |

Tractor Guidance and Autosteer Technology for Large Tractors |

2.6. |

Auto steer for large tractors |

2.7. |

Ten-year forecasts for autosteer tractors |

2.8. |

Master-slave or follow-me large autonomous tractors |

2.9. |

Fully autonomous driverless large tractors |

2.10. |

Fully autonomous unmanned tractors |

2.11. |

Technology progression towards driverless autonomous large-sized tractors |

2.12. |

Handsfree Hectar: fully autonomous human-free barley farming |

2.13. |

Tractors evolving towards full autonomy: 2018-2038 market forecasts in unit numbers segmented by level of navigational autonomy |

2.14. |

Tractors evolving towards full autonomy: 2018-2038 market forecasts in market value segmented by level of navigational autonomy |

2.15. |

Tractors evolving towards full autonomy: 2018-2038 market forecasts segmented by level of navigational autonomy (value of automation only) |

3. |

AUTONOMOUS ROBOTIC AGRICULTURAL PLATFORMS |

3.1. |

Autonomous small-sized agricultural robots |

3.2. |

FENDT (AGCO) launches swarms of autonomous agrobots |

3.3. |

Autonomous agricultural robotic platforms |

4. |

AUTONOMOUS ROBOTIC WEED KILLING |

4.1. |

From manned, broadcast towards autonomous, ultra precision de-weeding |

4.2. |

Crop protection chemical sales per top suppliers globally |

4.3. |

Sales of top global and Chinese herbicide suppliers |

4.4. |

Global herbicide consumption data |

4.5. |

Glyphosate consumption and market globally |

4.6. |

Regulations will impact the market for robotic weed killers? |

4.7. |

Penetration of herbicides in different field crops |

4.8. |

Growing challenge of herbicide-resistant weeds |

4.9. |

Autonomous weed killing robots |

4.10. |

Autonomous robotic weed killers |

4.11. |

Organic farming |

4.12. |

Robotic mechanical weeding for organic farming |

4.13. |

Technology progression towards autonomous, ultra precision de-weeding |

4.14. |

The rise of fleets of small autonomous robots: 2018-2038 market forecasts in unit numbers segmented by level of robot functionality |

4.15. |

The rise of fleets of small autonomous robots: 2018-2038 market forecasts in market value segmented by level of robot functionality |

5. |

ROBOTIC IMPLEMENTS: WEEDING, VEGETABLE THINNING, AND HARVESTING |

5.1. |

Autonomous lettuce thinning robots |

5.2. |

Why asparagus harvesting should be automated |

5.3. |

Automatic asparagus harvesting |

5.4. |

Robotic/Automatic asparagus harvesting |

5.5. |

Addressable market size for robotic lettuce thinning and weeding service provision |

5.6. |

Robotic tractor-pulled implements become increasingly intelligent and multi-functional: 2018-2038 market forecasts |

6. |

ROBOTIC FRESH FRUIT PICKING |

6.1. |

Field crop and non-fresh fruit harvesting is largely mechanized |

6.2. |

Fresh fruit picking remains largely manual |

6.3. |

Machining aiding humans in fresh fruit harvesting have not evolved in the past 50 years |

6.4. |

Emerging robotic fresh fruit harvest assist technologies |

6.5. |

Robot orchard data scouts and yield estimators |

6.7. |

Robotic fresh apple harvesting |

6.8. |

Fresh fruit harvesting robots |

6.9. |

Technology and progress roadmap for robotic fresh fruit harvesting |

6.10. |

Addressable market size for robotic fresh apple-picking service provision |

6.11. |

Robotic fresh fruit harvesting will overcome challenges but only in the long run: 2018:2038 market forecasts for robotic fresh fruit harvesting |

6.12. |

Robotic fresh strawberry harvesting |

6.13. |

Evolution of fresh strawberry harvesting robots |

6.14. |

Fully autonomous strawberry picking robots with soft grippers |

6.15. |

Addressable market size for robotic fresh strawberry-picking service provision |

6.16. |

Ten-year market forecasts for robotic fresh strawberry harvesting by territory |

7. |

VINE PRUNING ROBOTS |

7.1. |

Autonomous robotic vineyard scouts and pruners |

8. |

GREENHOUSES AND NURSERIES |

8.1. |

Autonomous robotics for greenhouses and nurseries |

9. |

ROBOTIC SEEDERS |

9.1. |

Variable rate technology for precision seed planting |

9.2. |

Robotic seed planting |

10. |

ROBOTIC DAIRY FARMING |

10.1. |

Global trends and averages for dairy farm sizes |

10.2. |

Global number and distribution of dairy cows by territory |

10.3. |

Robotic milking parlours |

10.4. |

Overview of robotic milking parlours |

10.5. |

Autonomous robotic feed pushers |

10.6. |

Alternatives to autonomous robotic feed pushers |

10.7. |

Autonomous robotic shepherds |

10.8. |

Autonomous manure cleaning robots |

10.9. |

Ten-year market forecasts for robotic milking systems by country |

10.10. |

Robotic milking are already a major market: 2018-2038 market forecasts |

11. |

AERIAL DATA COLLECTION AND DRONES |

11.1. |

Drones: dominant designs begin to emerge |

11.2. |

Drones: moving past the hype? |

11.3. |

Drones: company formation slows down |

11.4. |

Drones: global geographical spread of companies |

11.5. |

Drones: platforms commoditize? |

11.6. |

Drones: market forecasts |

11.7. |

Drones: application pipeline |

11.8. |

Satellite vs plane vs drone mapping and scouting |

11.9. |

Benefits of using aerial imaging in farming |

11.10. |

Unmanned drones in rice field pest control in Japan |

11.11. |

Unmanned drones and helicopters for field spraying |

11.12. |

Unmanned agriculture drones on the market |

11.13. |

Comparing different agricultural drones on the market |

11.14. |

Regulation barriers coming down? |

11.15. |

Agricultural drones: the emerging value chain |

11.16. |

Core company information on key agricultural drone companies |

11.17. |

Software opportunities: Vertical focused actionable analytics |

11.18. |

Drones: increasing autonomy |

11.19. |

Ten-year market forecasts for agricultural drones |

12. |

ENABLING TECHNOLOGIES: GRIPPER TECHNOLOGY |

12.1. |

Suction-based end effector technologies for fresh fruit harvesting |

12.2. |

Simple and effective robotic end effectors for fruit harvesting |

12.3. |

Soft robotics based end effector technologies for fresh fruit handling |

12.4. |

Pneumatic soft actuator: extensible layer + fiber |

12.5. |

Soft actuator: self-contained McKibbern-type muscle |

12.6. |

Shape Deposition Manufacturing (SDM) Compliant Joint |

12.7. |

Fabrication processes for soft robotic actuators |

12.8. |

Robotic end effector technologies for fresh fruit harvesting |

12.9. |

Dexterous robotic hands for agricultural robotics |

12.10. |

Examples of dexterous robotic hands |

13. |

ENABLING TECHNOLOGIES: NAVIGATIONAL TECHNOLOGIES (RTK, LIDAR, LASERS AND OTHERS) |

13.1. |

RTK systems: operation, performance and value chain |

13.2. |

Lidar- basic operation principles |

13.3. |

Review of LIDARs on the market or in development |

13.4. |

Performance comparison of different LIDARs on the market or in development |

13.5. |

Assessing suitability of different LIDAR for agricultural robotic applications |

13.6. |

Hyperspectral image sensors |

13.7. |

Hyperspectral imaging and precision agriculture |

13.8. |

Hyperspectral imaging in other applications |

13.9. |

Hyperspectral imaging sensors on the market |

13.10. |

Common multi-spectral sensors used with agricultural drones |

13.11. |

GeoVantage |

13.12. |

Why is new robotics becoming possible now? A hardware point of view |

13.13. |

Why is new robotics possible now? |

13.14. |

Transistors (computing): price evolution |

13.15. |

Transistors (computing): performance evolution |

13.16. |

Memory (RAM, hard driver and flash): price evolution in $/Mbit |

13.17. |

Memory: performance evolution in Gbit/ sq inch |

13.18. |

Sensors (Camera): price evolution |

13.19. |

Sensors (MEMS): price evolution |

13.20. |

Sensors (GPS): price and market adoption (in unit numbers) evolution of GPS sensors |

13.21. |

Is Lidar on a similar path as other robotic sensor technologies? |

13.22. |

Li ion battery: performance evolution in Wh/Kg and Wh/L |

13.23. |

Energy storage technologies: price evolution in $/kWh by sector |

13.24. |

Electric motors: evolution of size of a given output since 1910 |

13.25. |

Artificial intelligence: waves of development |

13.26. |

Terminologies explained: AI, machine learning, artificial neural networks, deep neural networks |

13.27. |

Rising interesting in deep learning |

13.28. |

Algorithm training process in a single layer |

13.29. |

Towards deep learning by deepening the neutral network |

13.30. |

The main varieties of deep learning approaches explained |

13.31. |

Evolution of deep learning |

13.32. |

The rise of the big data quantified: fuel for deep learning applications |

13.33. |

Examples of milestones in deep learning AI: word recognition supresses human level |

13.34. |

Deepening the neutral network to increase accuracy rate |

13.35. |

GPUs: an enabling component for deep learning? |

13.36. |

Examples of milestones in deep learning AI: translation approaching human level performance |

13.37. |

Examples of milestones in deep learning AI: leap in progress in robotic grasping |

13.38. |

What is 'good enough' accuracy in deep learning? |

13.39. |

RoS and RoS-I: major open source movement slashing development costs and enticing OEMs to finally engage |

13.40. |

Robotic Operating System (RoS): Examples of cutting edge projects |

14. |

COMPANY INTERVIEWS AND PROFILES |

14.1. |

Interview based company profiles |

14.1.1. |

Agrobot |

14.1.2. |

Blue River Technology |

14.1.3. |

DeepField Robotics |

14.1.4. |

F. Poulsen Engineering ApS |

14.1.5. |

Fresh Fruit Robotics |

14.1.6. |

Harvest CROO Robotics |

14.1.7. |

Ibex Automation |

14.1.8. |

miRobot |

14.1.9. |

Naio Technologies |

14.1.10. |

Nippon Signal |

14.1.11. |

Parrot |

14.1.12. |

Precision Hawk |

14.1.13. |

Quanergy |

14.1.14. |

Robotic Solutions |

14.1.15. |

Shadow Solutions |

14.1.16. |

Soft Robotics Inc |

14.1.17. |

Stream Technologies |

14.1.18. |

SwarmFarm Robotics |

14.1.19. |

Tillet and Hague |

14.1.20. |

Velodyne LIDAR |

14.2. |

Company Profiles |

14.2.1. |

3D Robotics |

14.2.2. |

AGCO |

14.2.3. |

AgEagle |

14.2.4. |

AgJunction Inc |

14.2.5. |

Agribotix |

14.2.6. |

Airinov |

14.2.7. |

Autonomous Tractor Cooperation |

14.2.8. |

Beijing UniStrong Science and Technology (BUST) |

14.2.9. |

Case IH |

14.2.10. |

Dogtooth Technologies |

14.2.11. |

Empire Robotics |

14.2.12. |

Farmbot |

14.2.13. |

Festo Gamaya |

14.2.14. |

GrabIT |

14.2.15. |

Harvest Automation |

14.2.16. |

Headwall |

14.2.17. |

HerdDog |

14.2.18. |

HETO |

14.2.19. |

HiPhen |

14.2.20. |

Hortau |

14.2.21. |

John Deere |

14.2.22. |

Kinzes Autonomous Harvest System |

14.2.23. |

Kubota Corp |

14.2.24. |

L'Avion Jaune |

14.2.25. |

LeddarTech |

14.2.26. |

Lely |

14.2.27. |

LemnaTec |

14.2.28. |

Magnificant |

14.2.29. |

Mavrx |

14.2.30. |

McRobotic |

14.2.31. |

MicaSense |

14.2.32. |

Motorleaf |

14.2.33. |

NavCom |

14.2.34. |

Near Earth Autonomy |

14.2.35. |

Novariant |

14.2.36. |

Orbital Insight |

14.2.37. |

Pix4D |

14.2.38. |

Prospera |

14.2.39. |

Qubit Systems |

14.2.40. |

Robotics Plus |

14.2.41. |

Robotnik |

14.2.42. |

Scanse |

14.2.43. |

senseFly |

14.2.44. |

Sentra |

14.2.45. |

SkySquirrel |

14.2.46. |

SpelR |

14.2.47. |

Trimble |

14.2.48. |

UAV-IQ Precision Agriculture |

14.2.49. |

Urban Crops |

14.2.50. |

URSULA Agriculture |

14.2.51. |

VineRangers |

14.2.52. |

Yanmar |

14.2.53. |

Yara |

|

|

|

ENABLING TECHNOLOGY: SOFTWARE, DEEP LEARNING AND BIG DATA |

|

TABLES AND FIGURES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Ten-year market forecasts for agricultural drones |

Source: IDTechEx