Dovly AI Review 2026: Can You Really Build or Fix Your Credit Score With AI? (Find Out!)

New data highlights how AI-driven credit platforms are being evaluated by consumers seeking structured credit improvement, monitoring, and identity protection solutions

NEW YORK, April 18, 2026 (Newswire.com) - Some links are affiliate links, which means a commission may be earned at no additional cost to you. This content is for informational purposes only and does not constitute financial, legal, or credit-repair advice. Under federal law, you have the right to review your credit reports and dispute inaccuracies directly with credit reporting companies at no cost.

Dovly AI Platform Expands Awareness Around Automated Credit Monitoring, Dispute Support, and Credit-Building Tools in 2026

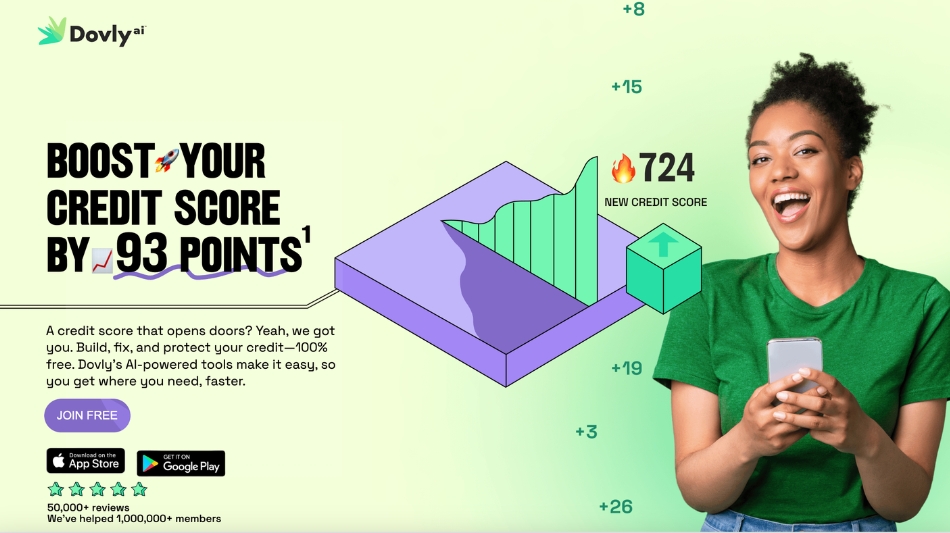

You just saw an ad for Dovly AI - maybe on Instagram, Facebook, or YouTube - that claimed the app can raise your credit score by 93 points. Now you're here, doing what any smart person does before they hand over their personal information or their money: you're trying to figure out if that claim is actually real.

That is the right move. The credit improvement space is full of services that make big promises, charge a monthly fee, and disappear into the background while your score goes nowhere. Your skepticism is earned, and this guide respects it.

Here is what you are going to get: a clear explanation of exactly how Dovly AI works, what the company's own published data shows about real member outcomes, what the free plan actually includes, what requires a paid subscription, and an honest look at who this is likely to help versus who might be better served by something else. No cheerleading. No pressure. Just the information you need to decide for yourself.

View Dovly AI details on the official website

What Dovly AI Actually Does

Dovly AI is an AI-powered credit platform that the company describes as a credit engine - a tool designed not just to tell you what your score is, but to actively work on moving it. According to Dovly's website, the platform has served more than 1,500,000 Americans.

The platform is built around four functions that most people with credit challenges typically need to address simultaneously: monitoring, dispute support, credit building, and identity protection. Most credit apps handle one of these. Dovly's design argument is that solving only one problem while the others remain unaddressed is why so many people end up frustrated with slow or inconsistent results.

That framing is worth understanding before you evaluate whether the app is right for your situation.

The Free Plan: Real, With Real Limitations

Dovly AI's free tier costs nothing and requires no credit card to sign up. According to the company's website, the free plan includes a monthly TransUnion credit report and score, manual dispute selection with TransUnion, a security score that shows your risk level, and limited data breach alerts.

The free plan produces real outcomes. According to Dovly's published data, a sample of 3,231 free members who remained enrolled for more than six months saw an average credit score increase of 38 points as of December 2025.

Thirty-eight points are meaningful. Depending on where you start and what you are applying for, that kind of movement can be the difference between an approval and a denial, or between a rate that makes sense and one that does not. The free plan is worth trying before you decide on anything about the paid tier.

There are honest limitations, though. The free plan gives you one manual dispute selection with TransUnion per month. You choose what to dispute, and the platform facilitates and helps automate dispute submissions through TransUnion. But the AI-powered automation, credit-building tools, weekly reports, identity theft protection, and the full monitoring layer all require Premium.

The Premium Plan: What Changes and What It Costs

Dovly AI Premium is $39.99 per month, or $99.99 per year - which works out to $8.33 per month on the annual plan - according to the company's official website. The company's FAQ states that subscriptions can be canceled at any time with no cancellation fees or penalties.

The upgrade from free to Premium is not minor. The difference in outcomes in Dovly's own published data is large. A sample of 2,922 Premium members who remained enrolled for more than six months saw an average credit score increase of 93 points as of December 2025.

To be direct about what that means: this is a company-reported average from a defined sample group. It reflects what those particular members experienced during that period. It is not a guarantee of what any individual user will experience. The company's own disclosures note that every case is different, that results vary based on credit profile and level of engagement, and that not everyone will achieve the same outcomes. That transparency from the company is worth acknowledging, and it should inform how you read that number.

Here is what Premium adds over the free tier, according to Dovly's official website:

Weekly TransUnion credit reports and scores replace the monthly reports in the free plan. Unlimited AI-powered dispute support with TransUnion, replacing the single manual dispute selection. Real-time monitoring alerts you when changes occur to your credit file. TransUnion credit lock, which lets you restrict access to your TransUnion file when you are not actively applying for credit. Up to $1 million in identity theft insurance, subject to the terms of the provider's policy. And access to the credit-building tools, which are the most distinctive part of this platform.

How the Credit Building Tools Work

This is where Dovly AI differs most clearly from basic monitoring services, and it is worth understanding carefully because the two building tools report to different bureaus.

The $2,000 Tradeline

According to Dovly's credit builder page, when you activate the tradeline feature as a Premium member, a $2,000 tradeline is added to your credit report. Every on-time monthly payment is then reported to Experian.

A tradeline is simply a credit account listed on your report. Adding this one increases your total available credit. If your balances stay the same, your credit utilization ratio drops - and credit utilization is one of the most significant factors in how scoring models calculate your score, typically representing a substantial portion of the overall calculation. Lower utilization generally means a higher score, all else being equal.

What you are not doing here is borrowing money or spending anything. You make a flat monthly payment, which is reported as on-time history to Experian, and the $2,000 appears as available credit on your file. Eligibility is subject to approval and enrollment completion, according to the company's terms.

The Bill-Reporting Builder

The bill-reporting builder works differently. According to Dovly's published site, this tool reports your rent, telecom, and utility payments - payments you are likely already making - through Dovly's reporting partners, with reporting reflected primarily via TransUnion-based reporting, according to the company's public pages. It can add up to 24 months of past on-time payment history retroactively.

That retroactive piece is significant. If you have been paying rent on time for two or three years and none of that history has ever appeared on your credit file, adding it now may produce a faster initial impact compared to dispute-based changes, depending on the individual credit file. Payment history is the single most important factor in most credit scoring models. For people with years of responsible payment behavior that credit bureaus have never seen, this tool allows that payment history to be reflected in their credit file.

The two building tools can be used simultaneously under a Premium membership. They are not automatically activated - you need to manually enroll in each one from your dashboard after signing up.

Important note on bureau reporting: based on Dovly's public pages, the tradeline reports to Experian while dispute support focuses on TransUnion. The bill-reporting builder reports through Dovly's reporting partners, with reporting reflected primarily via TransUnion-based reporting according to the company's public pages. Before enrolling, verify the current bureau coverage for each specific feature directly with Dovly, as these details can evolve.

How the AI Dispute Support Works

Credit report errors are more common than most people expect. Consumer research has found that a meaningful percentage of Americans have at least one inaccuracy on their credit reports - errors that can suppress scores without the person ever knowing they exist.

Dovly's AI reviews your credit report, identifies items that appear disputable, and the platform facilitates and helps automate dispute submissions through TransUnion on your behalf. Premium members receive unlimited dispute submissions, with the AI determining timing and sequencing based on the specifics of your file rather than sending everything at once.

There are things worth being clear about here, because the credit dispute landscape is confusing.

First, timing. The dispute process is not instant. Credit bureaus are legally required to investigate disputes within about 30 to 45 days. Results depend entirely on what the bureau finds when it investigates - not on what you submitted or what any service promises.

Second, what disputes can and cannot accomplish. Under the Fair Credit Reporting Act, inaccurate items, items that cannot be verified, and items that have exceeded their legal reporting time limit can be removed from your file. Accurate, verifiable negative information cannot be removed by anyone - not by Dovly, not by any credit repair company, not by an attorney. If a service tells you otherwise, that is not accurate. The common negative items that disputes can legitimately address include incorrect account statuses, balances that were settled but still show as delinquent, outdated collections past the seven-year reporting window, accounts that do not belong to you, and inquiries you did not authorize.

Third, the difference between automation and magic. What Dovly's AI handles is identifying which items in your report are potentially disputable, strategically sequencing submissions rather than flooding the bureau all at once, and tracking outcomes. The underlying legal process - the bureau's investigation - runs on the same timeline it would regardless of which service submitted the dispute.

Fourth, your rights regardless of which service you use. Under federal law, you have the right to dispute errors on your credit report directly with each credit reporting company at no cost. The Consumer Financial Protection Bureau provides free resources explaining exactly how to do this at consumerfinance.gov. Using Dovly is a way to automate and systematize the process. It is not the only path to accessing a right that exists independently of any paid service.

View current Dovly AI Premium pricing on the official website

The Identity Protection Layer

Dovly AI Premium includes continuous monitoring of your TransUnion credit file with real-time alerts when changes occur. This functions as an early warning system - if a new account appears in your name, if an inquiry you did not make shows up, or if a balance changes unexpectedly, you receive a notification.

The TransUnion credit lock feature lets you restrict access to your TransUnion file with a switch. When you are actively applying for credit, you unlock it. When you are not, you lock it, which prevents unauthorized new credit applications from being processed against your TransUnion data.

According to the company's website, Dovly AI Premium includes up to $1 million in identity theft insurance, subject to the terms of the provider's policy. Review the plan terms directly with Dovly for current coverage details.

According to Dovly's published site, the platform uses bank-level security in data transmissions and does not share or sell user data without consent.

Who Dovly AI Is Most Likely to Help

Dovly AI May Be a Strong Fit If You:

Have a specific financial goal within the next three to six months. Someone trying to qualify for a better mortgage rate, get approved for a car loan before a major sales event, or secure an apartment lease before a move-in deadline has a real reason to act now. The combination of tradeline addition, bill-reporting history, and automated dispute support addresses multiple score factors simultaneously, which matters when time is limited.

Have credit report errors you have not addressed. If you have never specifically reviewed your credit file for inaccuracies, there is a statistically real chance something is wrong. The automated dispute process removes the need to understand credit law, draft letters, or track bureau responses yourself.

Are building from a thin credit file or a score below 600. According to Dovly's published data, 96 percent of members with a credit score below 550 saw a score improvement in a sample of 8,687 Build product users as of March 2025. The tradeline and bill-reporting tools are specifically relevant for people who have little credit history rather than just damaged credit - these are genuinely different problems that require different solutions.

Want automation rather than manual management. The platform handles dispute sequencing, payment reporting, and monitoring in the background. For someone who finds the credit bureau process confusing, time-consuming, or simply not something they want to spend time on, this degree of automation has genuine practical value.

Are weighing cost against alternatives. The free tier produces real outcomes with no financial commitment. The annual Premium plan works out to $8.33 per month, according to the official website.

Dovly AI May Not Be the Best Fit If You:

Need multi-bureau dispute coverage as your primary need. Dovly's dispute support infrastructure focuses on TransUnion. If significant problems exist on your Equifax or Experian files and active dispute management is your main goal, evaluating whether Dovly's coverage matches your specific need is important before committing.

Already have a strong credit score with no errors. If you are in the mid-700s or above with no meaningful inaccuracies and no significant utilization issues, the active improvement tools are less directly relevant. The free monitoring tier may serve your needs without a Premium subscription.

Are looking for a one-time intervention rather than ongoing enrollment. The outcome data Dovly publishes reflects members who stayed enrolled for six months or longer. Credit improvement through dispute resolution, tradeline building, and payment history reporting is a process that compounds over time. People seeking a quick single-event fix may be disappointed regardless of which platform they use.

Prefer full transparency into every step. Because Dovly's AI handles dispute sequencing and submission automatically, you do not see every specific letter or communication sent to the bureaus. Someone who wants to review and approve every action taken on their behalf may prefer a more manual approach.

Questions Worth Asking Yourself Before You Decide

Is your credit score currently preventing something specific - a loan approval, a better rate, an apartment application?

Do you know for certain whether there are errors on your credit report, or have you simply assumed there are not?

Which credit bureau is your next lender or landlord most likely to pull - and does the coverage Dovly provides match that need?

Are you in a position to stay enrolled for several months, or are you looking for something with immediate one-time results?

Have you already tried disputing errors yourself directly through the bureaus at no cost?

Your answers to these questions will tell you more about whether Dovly is the right tool for your specific situation than any review can.

If your score is currently below 650 and you have a specific financial goal in the next six months, it may be reasonable to consider starting with the free tier. If your score is already healthy, your credit file has no meaningful errors, and your main interest is awareness rather than active improvement, a free monitoring tool may be all you need. The gap between those two situations is where most of this decision lives, and you know your situation better than any article does.

How to Get Started

Enrollment takes under two minutes according to the company, and does not require a hard credit pull. Signing up does not affect your credit score.

To enroll, you must be at least 18 years old, a U.S. resident, and have a valid Social Security number. Identity verification is required and may include a photo ID. The service is available in all 50 U.S. states, the District of Columbia, and all five major U.S. territories.

After enrollment, the AI reviews your credit report and provides a personalized action plan. The credit-building features - the tradeline and the bill-reporting builder - are not activated automatically. You enroll in each manually from your dashboard once you have reviewed your plan.

For questions, according to the company's website, customer support is available through the contact page at dovly.com/contact/.

The Bottom Line

Dovly AI is a platform with a clear design logic: most credit problems involve multiple factors at once, and tools that only address one of them produce partial results. The combination of automated dispute support with TransUnion, a credit-building tradeline that reports to Experian, retroactive bill-payment reporting, real-time monitoring, and identity protection under one subscription addresses that multi-factor problem in a way that most single-purpose credit apps do not.

The 93-point average improvement that appears in the ad is a real data point from a real sample of real members. It is also an average from a specific group of people enrolled for six months or longer - not a guaranteed outcome for every user. The company discloses this clearly in its own footnotes. Read those footnotes. The free plan requires no payment information and gives the AI a chance to review your file before you make any commitment.

If your situation is more complex - errors to dispute, no credit history to speak of, utilization pulling your score down - the Premium tier addresses all of those together. The annual cost is modest compared to what a meaningful score improvement is worth over the life of a mortgage, a car loan, or even a single year of better interest rates on existing credit.

Whether this is the right tool for you depends on what your credit file actually looks like and what you need it to do. The only way to know that is to let the platform analyze your file, which the free tier lets you do at no cost and with no impact to your credit score, according to the company.

Frequently Asked Questions

Is the 93-point increase in the Dovly AI ad actually real?

According to Dovly's published footnotes, the 93-point figure is an average increase experienced by a sample of 2,922 Premium members enrolled for more than six months, as of December 2025. It is a real data point from a real sample, not a number invented for advertising. It is not a guarantee. The company states explicitly that every case is different and results vary by individual.

Does signing up for Dovly AI hurt your credit score?

According to Dovly's website, enrollment does not require a hard credit pull and will not affect your credit score.

Is Dovly AI actually free? The free tier is genuinely free with no credit card required. It includes a monthly TransUnion report and score and one manual dispute selection per month. The features that drive larger outcomes - unlimited AI-powered dispute support, credit building, weekly reports, identity protection - require the paid Premium subscription.

Which credit bureaus does Dovly AI work with?

According to Dovly's published pages, dispute support focuses on TransUnion, where reports and scores are also provided. The $2,000 tradeline builder reports payments to Experian. The bill-reporting builder reports rent, telecom, and utility payments through Dovly's reporting partners, with reporting reflected primarily via TransUnion-based reporting according to the company's public pages. Verify current bureau coverage for each specific feature directly with Dovly before enrolling, as operational details can change.

Can Dovly AI remove accurate negative information from my credit report?

No, and no service can. Under the Fair Credit Reporting Act, accurate and verifiable negative information stays on your report for its legally defined reporting period regardless of what any service does. What dispute services can accomplish is the removal of inaccurate items, items that cannot be verified, and items that have exceeded their legal reporting window. You also have the right to dispute errors directly with the credit bureaus at no cost.

How long does it take to see results?

According to Dovly's FAQ, timelines vary. Members using the bill-reporting builder may see an initial impact more quickly than dispute-based changes when past payment history is added retroactively, though outcomes depend on the individual credit file. The tradeline typically shows its first impact within about 30 days. Dispute-based results depend on bureau investigation timelines. The company notes that many members see double-digit score changes within four months, with results depending on individual credit history and engagement.

Can I cancel Dovly AI at any time?

According to the company's FAQ, yes - subscriptions can be canceled at any time with no cancellation fees or penalties.

How much does Dovly AI Premium cost?

According to Dovly's official website, Premium is $39.99 per month on the monthly plan, or $99.99 per year - equivalent to $8.33 per month - on the annual plan.

Can I dispute my own credit report errors without Dovly?

Yes. Under federal law, you have the right to dispute inaccuracies on your credit report directly with each credit bureau at no cost. The Consumer Financial Protection Bureau provides free guidance on how to do this. Dovly automates and systematizes the process; it does not provide access to a right that only paid services offer.

How many people use Dovly AI? According to the company's website, Dovly AI has helped more than 1,500,000 Americans take control of their credit scores.

View Dovly AI details on the official website

Contact Information

Email: support@dovly.com

Disclaimers

Advertorial and Affiliate Disclosure: This is paid sponsored content. Compensation may received if you click links or enroll through links in this article. Some links are affiliate links, which means a commission may be earned at no additional cost to you. This compensation does not influence the accuracy, neutrality, or integrity of the information presented.

No Financial or Legal Advice: This content is for informational purposes only and does not constitute financial, legal, or credit-repair advice. Nothing in this article should be interpreted as a recommendation to take any specific financial action. Consult a qualified financial or legal professional for guidance specific to your situation.

Results May Vary: Individual results will vary based on starting credit score, credit history, the type and number of items on the credit file, level of engagement with the platform, consistency of use, and other individual factors. The averages cited in this article are company-reported figures from defined sample groups published by Dovly, Inc.: the 93-point average is based on a sample of 2,922 Dovly AI Premium members enrolled for more than six months as of December 2025; the 38-point average is based on a sample of 3,231 Dovly AI Free members enrolled for more than six months as of December 2025. These figures do not represent guaranteed outcomes for any individual user. People who write reviews are self-selected - members with positive experiences are more likely to submit feedback than those with neutral or mixed results.

Your Rights Under Federal Law: Under the Fair Credit Reporting Act, you have the right to obtain a free copy of your credit report from each of the three major credit bureaus once every twelve months through AnnualCreditReport.com. You also have the right to dispute inaccurate or incomplete information on your credit report directly with the credit reporting companies at no cost. The Consumer Financial Protection Bureau provides free resources about these rights at consumerfinance.gov.

Pricing Disclaimer: All pricing, promotional offers, and plan details were accurate based on publicly available information at the time of publication (April 2026) and are subject to change without notice. Always verify current pricing and terms directly on the official Dovly AI website at dovly.com before enrolling.

Publisher Responsibility: The publisher has made every effort to ensure accuracy at the time of publication based on publicly available information from Dovly, Inc.'s official website. We do not accept responsibility for errors, omissions, or outcomes resulting from the use of the information provided. Verify all details directly with Dovly, Inc. before making any decisions.

SOURCE: Dovly.ai

Source: Dovly.ai